The Dawn of Betting IntelligenceA Primer on Extracting Intelligence from Prediction Markets

Introduction: Gradually Then Suddenly

When we began publishing BetBreakingNews in September 2025, the idea that geopolitical prediction markets posed structural national security risks was still niche. When we were invited to speak at the McCain Institute earlier this year, many senior national security professionals openly acknowledged this was a new domain of thought for them.

Then came the capture of Venezuelan leader Nicolas Maduro and the resulting speculation that an insider who knew the attacks were going to happen profited off of that classified information.

That episode became the first true mainstream inflection point. Media outlets and policymakers began treating prediction markets not as curiosities, but as potential insider-threat and national security vectors.

Rep. Ritchie Torres introduced legislation aimed at restricting insider trading by members of Congress and executive branch officials on prediction platforms. Six senators led by Adam Schiff called for banning contracts “involving deaths.” During the same period, thoughtful analyses by Alex Goldenberg and Matthew Wein further mapped how war-focused markets could be weaponized and explored regulatory responses.

However, the true dawn of Betting Intelligence (BETINT) where media, policymakers, and the public turned to prediction markets as a primary source for geopolitical tracking arrived with the buildup and anticipation of a U.S. strike on Iran.

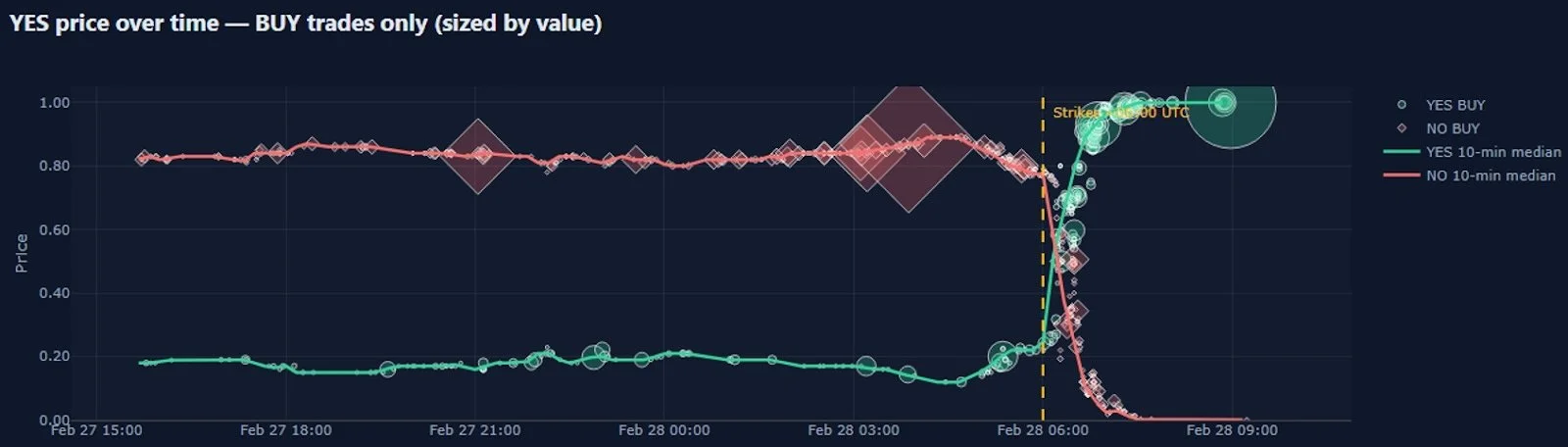

Chart via internal systems showing Iran strike markets. Size of the data bubble denotes the size of the bet placed. Note times in UTC (6AM UTC = 1AM ET)

For weeks, traders and observers watched markets asking whether and when the United States would act. Prices oscillated through multiple false starts. Then, around 11:30PM EST the evening before the strike, relevant Iran markets began climbing sharply. Public confirmation did not begin circulating until approximately 1:15AM on February 28.

That 90+ minute window marked a paradigm shift: market participants held the information long before newsrooms did. Yet, the ensuing commentary remained reductionist, centering primarily on two questions: “Who were the insiders?” and “Are these markets a net positive or negative?” (though let us compliment Aaron Courtney’s thorough layout of those elements and Rajiv Sethi’s look into how these markets treat the idea of profiting off of violence). These are necessary questions but there is even more to talk about with the market information.

These markets revealed far more than potential insider activity. They provided structured, time-stamped, incentive-layered data about expectations, positioning, and second-order risks. What we hope to do with this paper is provide a primer for decision makers who want to move toward disciplined interpretation of this data source.

What follows is a primer on the core operating principles of Betting Intelligence (BETINT). These are the foundational lenses we use when interpreting prediction markets in real-world crises.

Each principle can be read independently. Taken together, they form the early architecture of a broader research agenda - one that treats markets as structured, incentive-layered intelligence systems.

1. Start With the Question, Not the Data

Jumping into prediction market data without a clearly defined goal is a fundamental analytic error. Like any scientific or intelligence enterprise, Betting Intelligence (BETINT) requires a structured starting point. With tens of thousands of non-sports event contracts now live across various platforms, an analyst without a hypothesis will quickly drown in noise. Without a specific threat model or a clear understanding of your organizational exposure, the data is just a Rorschach test where you will simply see what you want to see.

Not every decision-maker cares about the same signals. If you are at FinCEN or the DOJ, your focus may be on insider identification and prosecution. If you are in the petroleum industry, you are likely searching for early indicators of kinetic events that move crude prices. If you are in defense, you may care more about operational timing and cascading retaliation, while a finance lead might prioritize volatility transmission across asset classes.

Different questions require different tradecraft. One field to turn to for possibilities is how intelligence professionals utilize structured analytical techniques like the Analysis of Competing Hypotheses (ACH) to remain objective. For example, if a single wallet wins $3 million on a geopolitical strike, you must weigh competing explanations: was it genuine insider knowledge, or was it a result of high-conviction open-source analysis, simple luck, wash trading, or even “signal jamming” (which we talk about more in later sections)?

By defining your hypotheses and the criteria for confirming them before touching the data, you avoid the lazy analysis of assuming every big winner is a mole. Other intelligence analysis methodologies and decision analysis tools can then be used to confirm or deny these theories but what matters is that you define hypotheses, classification criteria, and potential response actions before you immerse yourself in the data. Define the hypotheses first; only then do you collect the data.

2. Read the Rules. Every Word.

Market wording can be identical across platforms while tracking fundamentally different risks. The “Will Ayatollah Khamenei leave office?” contracts illustrate this: Polymarket allowed resolution via death, while Kalshi explicitly excluded it to avoid being classified as an “assassination market“. Because bettors prioritize profit, a Kalshi trader will not price in a kinetic resolution if the platform won’t pay out for it. Consequently, you cannot treat the data from these two platforms as a 1-to-1 comparison of the same reality.

And since we are on the subject of semantics, ambiguous wording creates both analytical distortion and legal exposure. This ambiguity creates incongruity of interpretation as different traders may connote the same contract differently. We foresee a future where specialized litigators exploit these linguistic loopholes for class action lawsuits. Controversial resolutions (like those surrounding Zelensky’s attire or Cardi B’s Super Bowl “performance”) are precursors to class-action lawsuits. When lawyers begin hunting for semantic ambiguities, the threat of litigation will force platforms to tighten rules, but until then, the “fog of the rules” remains a primary analytical hurdle.

3. Poly-Pump Fakes & Alarm Fatigue

In the weeks leading up to the February 28th strike, the information environment was defined by a series of false starts. Since mid-January, media chatter and prediction market spikes repeatedly suggested an attack was imminent, only for the odds to sharply deflate.

This scenario opens up for a technique we’ve previously written about called the Poly-Pump Fake, a technique where an actor seeks to create a false consensus by leveraging multiple information sources to profit from the resulting market volatility. While we don’t have confirmation that this was a deliberate White House directive, the tactical utility of such a maneuver in a monetized reality is undeniable.

This iteration of the Poly-Pump Fake leverages the same mechanics we’ve previously analyzed but shifts its objective to repeatedly pump faking the audience until it is time to actually go through with the action. By repeatedly triggering the market “alarm” without an ensuing “strike,” an actor induces alarm fatigue which is a phenomenon where the sheer frequency of alerts causes observers to become desensitized. Much like healthcare workers who eventually ignore critical monitors due to constant false positives, bettors and analysts habituated to “false starts” become the perfect victims of strategic surprise.

The hypothetical Poly-Pump Fake in this scenario has some other interesting elements to consider:

Narrative Weaponization: Repeated delays reinforced the “TACO” (Trump Always Chickens Out) narrative. Traders and analysts began to bake “inaction” into the price, assuming the administration was merely posturing about attacking.

Tactical Stealth: When Operation Epic Fury finally launched, the initial market movement was met with skepticism. Retail traders and betting intelligence analysts, conditioned by previous pump fakes, hesitated to react thus widening the window of tactical surprise for operational actors on the ground.

By keeping volatility just below the threshold of serious attention, a sophisticated actor can “cry wolf” until the adversary and the market stops listening. Sometimes volatility can be the ultimate camouflage.

4. Timing Often Matters More Than The Odds

In the Iran strike markets, price movements told only part of the story. Timing told the rest. Around 11:30 PM EST on February 27th, we observed a clustering of heavy, high-conviction “Yes” bets.

Screenshot from our own internal tool showing the timing of the volume of # of traders and the money volume for these Iran strike markets.

In national security and supply chain security, a 90 minute window can provide the lead time necessary for:

Asset Protection: Repositioning high-value personnel or hardening digital infrastructure against retaliatory cyberattacks.

Information Maneuver: Preparing a pre-emptive counter-narrative or a “rally around the flag” message before the adversary can frame the strike.

Operational Security: Identifying potential leaks by tracing the exact moment conviction entered the market relative to internal briefing cycles.

Remember that while the price/odds are likely the most important indicator for traders looking to profit, the “when” is usually much more important when it comes to actionable betting intelligence.

5. Don’t Ignore the Losing Side: Signal Jamming

A common analytical trap is focusing exclusively on the winning “Yes” bets. However, looking at the “losing” side is often more instructive for identifying counter-intelligence efforts and market manipulation.

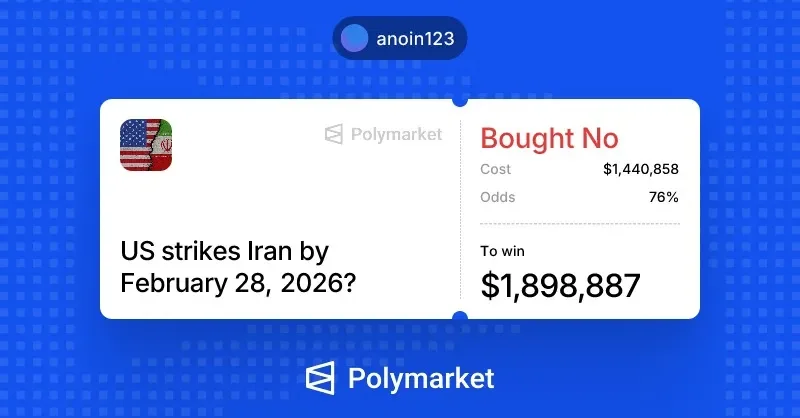

During the Iran strike buildup, we noticed many big “No” bets coming in about 5 hours before the market resolved to “Yes” (see screenshot from the Intro section) and we tracked a single position of over $1.4 million betting “No” on an imminent strike (see picture above). In a vacuum, this looks like a trader making a massive, incorrect bet (which it may very well be) but in an intelligence context, it forced our team to consider that it could be a technique our team calls Signal Jamming.

Just as electronic warfare units jam radar to mask a physical advance, a sophisticated actor can place massive, counter-intuitive bets to disrupt the market signal. When a government or insider has foreknowledge of a resolution, they have a powerful incentive to defray and obfuscate the BETINT value that other “sharps” might be extracting. Signal Jamming intentionally loses capital by flooding the order book and driving the price away from the market result a group is intending to happen. This serves to:

Mask Insiders: Dilute the impact of true insider “Yes” bets to prevent the price from moving too early and alerting adversaries.

Create Narrative Confusion: Mislead OSINT analysts, newsrooms, and competitors into believing the strike has been called off.

Economic Sabotage: Wipe out retail traders or opposing “sharks” who follow the “big money” into a trap.

We are only scratching the surface of this concept of signal jamming and we are considering making a longer article similar to our Poly-Pump Fake article to more fully explain it.

6. Not Every Insider is a Whale

When traders spot a suspiciously large position, the instinct is to assume the wallet belongs to an insider. However, the most sophisticated actors know how to hide their edge.

Polymarket’s most powerful differentiator from any betting platform that came before it is the fact that one person can have an unlimited amount of wallets linked to polymarket profiles. Practically, that means that a true insider could spread out their inside bet across 10, 50, 100+ wallets if they prioritize privacy which means a true insider can spread a million-dollar bet across hundreds of wallets. This is a form of insider trading that simple whale tracking systems are not built for but expect to see more “schools of minnow” in the near future after enough whales get caught.

Conversely, we must challenge the assumption that all insiders are high-net-worth oligarchs or executives. Insiders are often “everyday” individuals like a helicopter pilot, a low-level clerk, or a barracks technician who lack the capital to move the market but possess definitive operational knowledge.

Consider a servicemember who knows a strike is coming. They may not have $50,000 to wager, but they might deploy $500 through a cousin’s crypto wallet or a proxy account. While these “micro-bets” don’t shift the odds, they represent a significant moral and security failure. Betting that individuals will succumb to the “greed devil” is a more productive intelligence posture than assuming perfect institutional integrity.

7. Not Every Winner Is an Insider

While we have a proven track record of identifying genuine insider trading (see our work tracking the same insiders that led to Israeli authorities’ arresting IDF soldiers or the Institute for the Study of War (ISW) manipulated maps case), blanketly labeling every large winner an “insider” is lazy analysis.

The Iran strike scenario possessed a high Visibility Index, a composite metric we use to track open interest alongside media and social discourse frequency. High visibility naturally invites heavy retail participation and high-conviction “sharps” who synthesize open-source data more effectively than the average observer. When a scenario has weeks of mainstream buildup, the probability of “retail” being the primary driver increases.

Distinguishing between a lucky trader and a mole requires tradecraft that moves past basic blockchain tracing into behavioral profiling and attribution. To assess insider probability, we utilize a multi-variable assessment:

Media Visibility Metrics: Does the trade timing correlate with media and public discourse spikes?

Volume and Liquidity Depth: Did the trade “crash” the price or fill naturally within existing depth?

Unique Trader Counts: Was the price moved by a “crowd” or a coordinated “cluster”?

Cross-Platform Price Convergence: Do regulated and offshore prices align, or is one “leading” the other?

Historical Performance: Does the wallet consistently “guess” correctly across unrelated geopolitical events?

While we are developing advanced attribution tools for our platform to map wallets to persons, the immediate lesson for the decision-maker is caution: market visibility often explains what looks like an “inside” edge.

8. Mapping Correlating Markets Before They Happen

A common mistake in interpreting prediction markets is treating each event as isolated rather than as a node in a network of cross-correlated markets. After the Iran strike, for example, correlated markets moved in the Strait of Hormuz, oil-linked contracts, Bitcoin pricing, and even how many times Elon Musk will tweet this week.

Serious BETINT practitioners should aim to pre-map likely second- and third-order markets before a primary event resolves. We are currently developing tools to identify and test cross-market correlations and causality where we overlay multiple layers: open interest, cross-platform pricing, media chatter, and historical response patterns. The resulting correlation maps highlight which markets are likely reactionary, which are predictive, and where anomalies suggest potential insider influence or strategic manipulation. By structuring these dependencies in advance, analysts move from reactive observation to predictive insight, translating raw market data into forward-looking intelligence.

9. New Market Creation Is Signal

Markets rarely appear randomly; they are typically timed around anticipated events, insider knowledge, or heightened public interest. When a new contract appears, the first analytical question must be “Why now?”.

Months ago, the “Will Israel attack Yemen?“ market appeared roughly one week before real-world operations began. The creation timestamp and the speed at which liquidity filled were indicators we paid attention to on top of when we started to see insider betting action.

“When” the markets are created will become even more critical with the rise of permissionless markets, which are platforms where any user (not just the prediction market operator) can deploy a question if they provide the liquidity. Polymarket developers have already alluded to this shift, and some traders have claimed early access. Suffice it to say that Polymarket offering permissionless markets would lead to the same kinds of threats mentioned in headlines about prediction markets coming to a neighborhood near you.

Polymarket currently does list the date each market is created, including different time horizons on the same event. Pay close attention to these timestamps as valuable data.

10. Account for the Cultural and Spiritual Artifacts

Human behavior often follows cultural logic and dates matter. The strike on Iran coincided with the Jewish holiday of Purim; North Korea launching intercontinental ballistic missiles on July 4th, and our team has noted that President Trump has frequently announced/conducted major initiatives on Fridays after the stock market has closed.

Rationality is culturally bounded and why people do certain actions or choose certain days to do something could be with a logic that is wrapped up in cultural or spiritual reasons and it is on the betting intelligence analyst to be aware of these elements to best model/predict what could happen. Ignoring these artifacts risks misreading signals (even if they are seen as “superstitious”), while incorporating them allows analysts to detect subtle cues embedded in price movements and emerging contracts.

11. Cross-Platform & Demographic Intelligence

Kalshi and Polymarket dominate English discourse, but platform ecosystems are fragmenting.

Users migrate based on incentives. Emerging platforms will cater to specific cultural, political, or demographic niches. Over time, attribution and demographic profiling will mature beyond self-reporting.

Future BETINT will involve:

Cross-platform arbitrage analysis

Demographic inference modeling

Geographic wallet clustering

Monitoring offshore and privacy-enhanced platforms

Each platform is a sensor. The closer the sensor is to the population you care about, the stronger the signal. Assuming today’s top prediction market platforms remain dominant is strategically naive.

Conclusion: As Dawn Breaks

The dawn of Betting Intelligence marks a fundamental shift in how information flows, decisions are made, and risks are assessed. Even two years ago, cable news was seen as the slower news source that people used to double check if something they saw online was real.

Today, prediction markets have become the primary source for real-time tracking, while online news sources are relegated to the role of lagging validators. For this shift to fully materialize, decision-makers and the public must become fluent in what Betting Intelligence can reveal.

This fluency is also a call for competency in seeing prediction markets for what they truly are in the context of geopolitics: a non-kinetic weapon. Experts in national security treat the information environment (which includes online social media) as a battlespace where wars are won or lost (see this paper by J.D. Maddox for an overview on this framing). In this frame, prediction markets act like a sniper’s laser scope; directing attention to specific actors, topics, or signals to extract information or leverage for profit. Today, these “scopes” focus on adversaries like Iran or China, but permissionless platforms will inevitably turn them inward. Imagine markets predicting when and where the next mass shooting or school shooting will occur in the U.S.; that’s a horrifying yet plausible future.

The ultimate trajectory of prediction markets is clear from Kalshi’s CEO: to “financialize everything.”

Much as the internet has absorbed all facets of information, prediction markets are poised to absorb reality itself. By developing fluency in Betting Intelligence, analysts, policymakers, and enterprise leaders can move from reactive observation to anticipatory insight, transforming raw market activity into actionable intelligence and, ultimately, a sharper understanding of the world before it unfolds. You reading this far is hopefully another step towards that better future.